AI Monetisation

The GPUs are bought. Now bill for intelligence.

Infrastructure is not a business model, & commercial execution is the missing layer.

AI infrastructure is being bought at speed: GPUs, data centres, sovereign cloud regions, inference endpoints, orchestration tools, and vertical AI applications.

The investment becomes a business when every unit of intelligence can be packaged, metered, governed, rated, billed, settled, and reconciled.

Telecom operators have seen this pattern before. They built world-class networks while too much of the value moved to someone else’s application layer. AI can repeat the same mistake unless the commercial engine is built into the operating model from the start.

The missing layer

Infrastructure is not a business model.

GPU capacity is necessary. It is also easy to commoditise. Data pipelines matter. Sovereign hosting matters. Model access matters. None of those automatically becomes revenue.

The missing layer is commercial execution: who consumes the intelligence, how usage is measured, how the offer is packaged, how the channel sells it, how partners are settled, how invoices are produced, and how leakage is found. Without that layer, AI infrastructure becomes another cost centre with an impressive dashboard.

Buyer questions

- What exactly are we selling: compute, tokens, workflows, outcomes, or applications?

- Can we meter consumption in real time?

- Can we bill AI usage next to connectivity, cloud, and managed services?

- Can partners resell or package the service safely?

- Can we reconcile revenue across infrastructure, model, workflow, and channel layers?

- Can finance see the margin by product, customer, partner, and vertical?

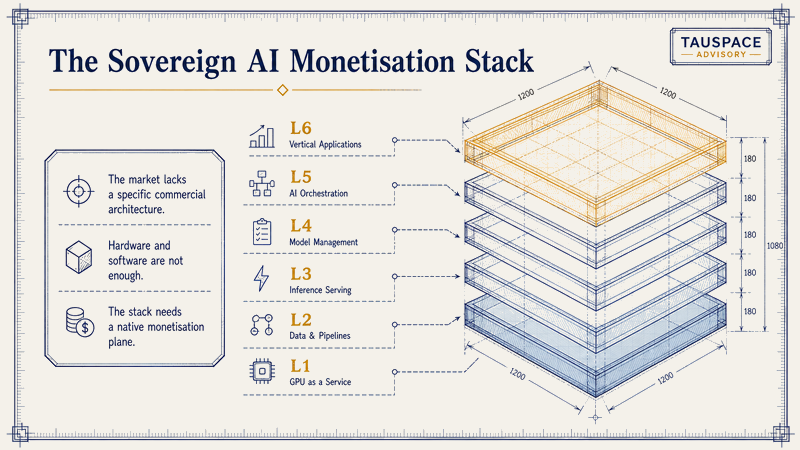

Six layers

Where does the margin move up the stack?

The AI investment becomes more defensible as it moves up the stack. The commercial model has to follow it, or the margin stays trapped in infrastructure rental.

Layer 01

GPU-as-a-Service

Necessary compute. Useful, but the easiest layer to commoditise.

Layer 02

Data and pipelines

Ingestion, ETL, vector stores, data movement, and pipeline governance.

Layer 03

Inference serving

Real-time model serving, metered by token, request, throughput, latency, or SLA.

Layer 04

Model management

Fine-tuning, hosting, versioning, lifecycle, and enterprise-specific model control.

Layer 05

AI orchestration

Multi-agent workflows, task routing, approvals, tool execution, and workflow billing.

Layer 06

Vertical AI applications

Domain applications billed by seat, event, transaction, workflow, outcome, or catalogue entry.

Two planes

Sovereignty protects it. Monetisation pays for it.

The market talks loudly about sovereign infrastructure. The harder question is who bills, reconciles, and assures the intelligence running on top of it. If the sovereignty plane is missing, the institution cannot defend the service. If the monetisation plane is missing, it cannot commercialise it.

Sovereignty plane

Data residency, encryption, tenant boundaries, model governance, approval gates, audit, and jurisdictional control.

Monetisation plane

Metering, rating, charging, billing, partner settlement, channel catalogue, revenue assurance, and invoice convergence.

Why operators have an advantage

Operators already own the trust fabric. That is not enough.

Telecom operators have assets many AI infrastructure players still have to rent: in-country data centres, fibre networks, spectrum, regulated operations, enterprise account relationships, billing history, field infrastructure, and carrier-grade support disciplines.

That creates a real advantage. But it only becomes a commercial advantage if the operator can turn AI into products customers can buy, partners can sell, and finance can recognise.

- enterprise account relationships

- existing contracts and billing relationships

- licensed and regulated operating posture

- in-country infrastructure and edge reach

- network and cloud bundles

- security, support, and managed-service capabilities

- channel and reseller relationships

Sovereign AI without metering, charging, billing, and channel packaging is still just expensive infrastructure.

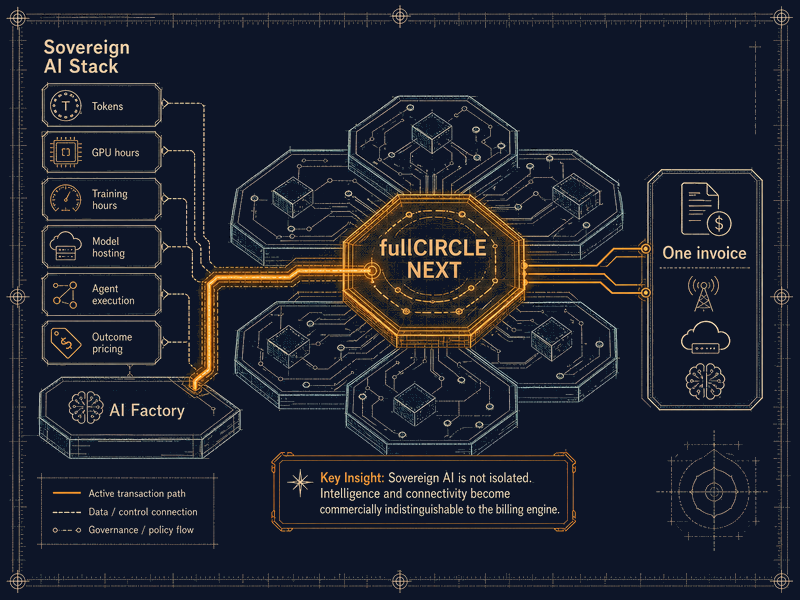

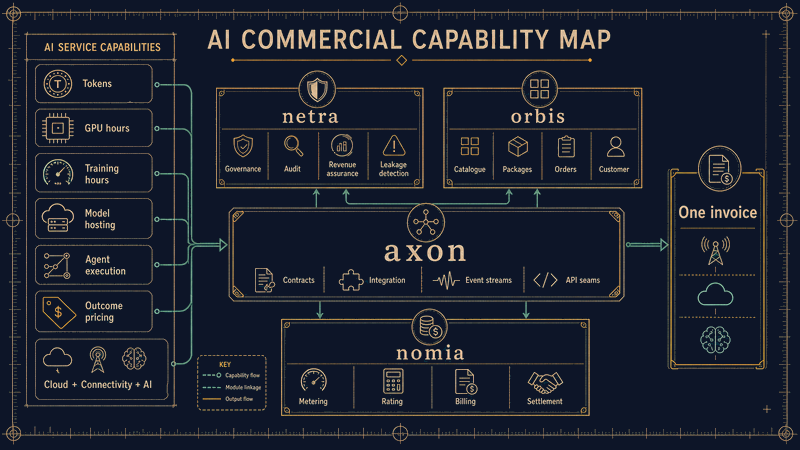

How fullCIRCLE NEXT monetises AI

Billing cannot be bolted on after the launch.

AI services need the same commercial discipline as telecom services: metering, rating, balance, billing, partner settlement, customer visibility, approval gates, revenue assurance, and reporting. fullCIRCLE NEXT was built for converged commercial operations. That matters when AI becomes one more service in the enterprise catalogue, sitting next to connectivity, cloud, security, managed services, and application subscriptions.

Capabilities mapped above

token and request metering · GPU-hour and training-hour billing · fine-tuning and model-hosting billing · workflow and agent execution billing · outcome-linked pricing · enterprise catalogue and package management · partner and channel settlement · revenue assurance and leakage detection · converged invoices across connectivity, cloud, and AI services.

Channel and partner enablement

The AI catalogue becomes the thing the channel can sell.

Direct AI consumption is only the first route to market. The bigger opportunity is the channel: enterprise teams, resellers, systems integrators, application providers, MVNEs, public-sector programmes, and vertical specialists who need a governed AI catalogue they can sell and support.

That requires more than access to a model. It requires catalogue control, role-based permissions, pricing, commissions, settlement, reporting, dispute handling, service levels, and customer evidence.

Channel capabilities

- reseller and partner catalogues

- enterprise AI bundles

- role-based partner access

- commission and revenue-share logic

- partner reporting

- wholesale AI packages

- vertical application listings

- service-level and entitlement rules

- partner settlement and reconciliation

The revenue path

Start where the first invoice can be proved.

The first move should not try to commercialise the whole AI stack. Start with the layer where the operating and commercial proof can be seen quickly, then climb from evidence.

Phase 1

Inference proof of value

One enterprise customer. Sovereign endpoint. Metered inference.

Commercial test: Can the service earn more than commodity infrastructure hosting?

Phase 2

Model management

Fine-tuning and model-hosting billing.

Commercial test: Can enterprise-specific model work be billed without losing data control?

Phase 3

Orchestration

Billable agent workflows with approval gates and audit trails.

Commercial test: Can workflows run in production and pass compliance review?

Phase 4

Vertical AI applications

AI applications in the catalogue. Channel and wholesale activation.

Commercial test: Can customers buy AI as a governed service, not raw infrastructure?

Caution. Treat the path above as a planning model. Real customer cases need their own evidence before any timing or outcome promise is made to the market.

Advisory support

The platform can bill it. The business still has to sell it.

The platform can meter and bill the service. The business still has to decide what to sell, which customer segment to start with, how the channel will work, how risk will be governed, and how pricing will survive contact with real consumption.

TAUSPACE advisory can help shape the business case, commercial model, channel operating model, product catalogue, partner terms, governance, and launch sequence.

The most GPUs will not decide this market.

The market will move to the organisation that can turn intelligence into a governed, billable, repeatable service.

Where this connects

Related work across the platform & advisory.

fullCIRCLE NEXT

The commercial fabric that meters, rates, bills, governs, and reconciles AI services next to connectivity, cloud, and managed services.

See the platformEnterprise & Channel Suite

Channel control, catalogue, settlement, and entitlement for AI services sold through partners.

See the SuiteCommercial advisory

Pricing, channel economics, partner terms, and commercial structure for AI services that survive contact with real customers.

See the practice